Buying a home involves more than just finding one you like…so, how long does it really take to buy a home?

Although current market trends can have some effect on how quickly you close on a home, the home-buying process typically is the same across the board. The only real difference is how long each phase in the process can take. In a buyer’s market, you might have the luxury to take your time to find an affordable home. While in a seller’s market, homes often get bought a lot faster to beat out potential competition.

So, how long does it actually take to buy a house? The home-buying journey begins the moment you decide you want to own a home! After that, the general timeframe for buying a home ranges from as short as a couple of months to as long as one year. It all depends on your preferences, your willingness to compromise, and your budget.

Looking to buy a house as quickly as possible? Check out our 90 Days to Homeownership guide to get in a new home in as little as three months! Interested in selling your home? Find out how long that process takes here.

To help you know what to expect when buying a home, we’ve identified each phase of the process and noted the typical amount of time it takes to complete. Whether you’re ready to buy a home now or simply curious about how long it would take, this complete timeline for buying a home will help you prepare and plan accordingly!

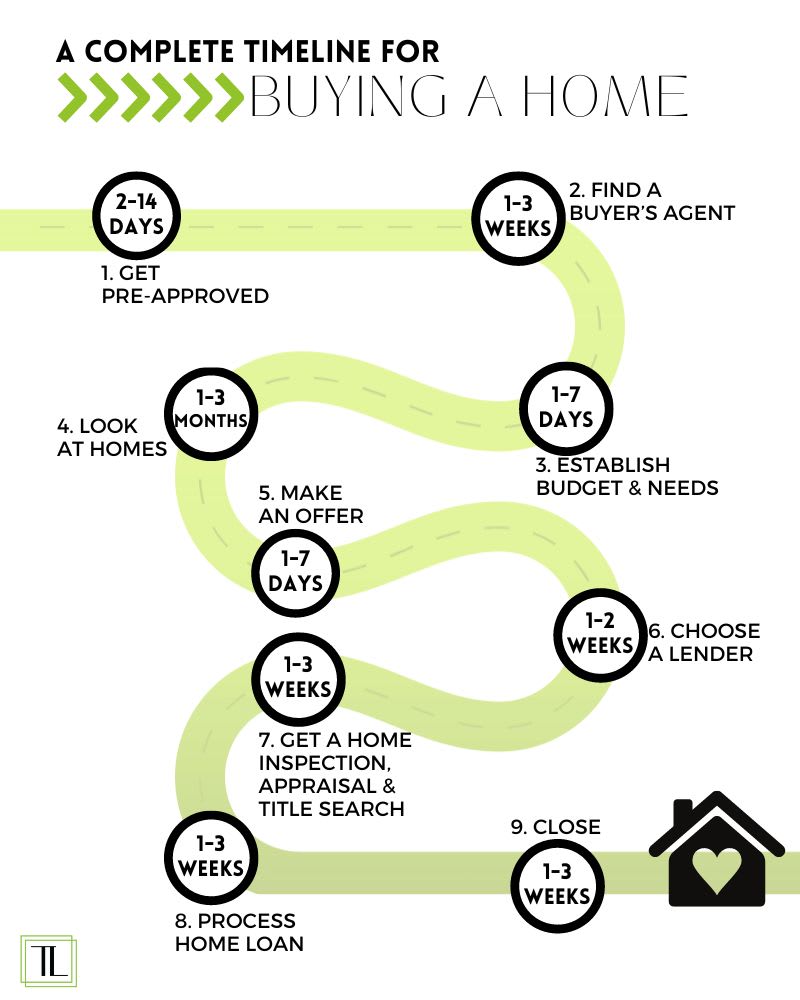

Timeline for Buying a Home:

- Get a mortgage pre-approval: 2-14 days

- Find a buyer’s agent: 1-3 weeks

- Establish your budget & needs: 1-7 days

- Look for homes: 1-3 months

- Make an offer & negotiate: 1-7 days

- Find a mortgage lender: 1-2 weeks

- Schedule the home inspection, home appraisal & title search: 1-3 weeks

- Process your home loan: 1-3 weeks

- Close: 3-10 days

Step 1: Get Pre-Approved to Buy a Home

Average timeline: Two days to two weeks

Once you’ve fully decided you’re ready to own a home, your first step should be reaching out to different mortgage lenders for pre-approval letters. A “mortgage pre-approval” is a letter stating the amount of money you’re qualified to borrow for a home loan. To come up with the pre-approval figure, lenders have to verify your finances and assets. It’s also a good idea to get a “proof of funds” letter, which shows you have enough cash to cover the down payment and other upfront costs associated with buying a home. If you have all the paperwork ready up front, you can save a considerable amount of time. Some of the documents you’ll be required to provide include:

- Proof of employment

- Recent pay stubs and W-2 forms

- Federal tax returns

- Bank and asset statements

- Credit report

- Residential history

While you don’t exactly have to be pre-approved before making offers on homes, it shows sellers you’re serious about buying a house and have the means to follow through with the purchase. Plus, it helps you set a more accurate budget!

Beware: pre-approval letters don’t guarantee a mortgage approval, they simply let sellers know you’re in good financial standing. In fact, you don’t even have to stick with the lender who pre-approves you, if you don’t want to! Also, they typically expire after 90 days. So, you’ll have to request a new one if you don’t buy a home in that timeframe.

Step 2: Find A Buyer’s Agent

Average timeline: Two days to several weeks. Or zero days if you check out our team of Houston real estate agents here.

Hiring a real estate agent to help you buy a home takes almost no time at all—you technically just have to sign a Buyer’s Representative Agreement—it can be a good idea for you to meet with a few different agents before picking one, especially if you’re a first time buyer.

After all, real estate professionals are not one-size-fits-all! Agents are humans too, and as with any profession, you may find you work better with one real estate professional over another. Or, you may find a buyer’s agent who has more experience with the type of real estate you’re looking to buy.

A buyer’s agent will not only help you find homes, but they’ll be your insight into neighborhoods and market trends; they’re your representative when communicating and negotiating with sellers; and they should be a trusted, reliable resource during closing.

Step 3: Set Your Budget & Goals for Buying a Home

Average timeline: One day to one week

Luckily, most real estate agents can help you identify your budget (if you haven’t already) and prioritize your goals as a homeowner. Maybe you need to 100% finance a home with more space or a big yard, or maybe you’re looking to buy a home as an investment opportunity—these things will help narrow down your home search and ensure you don’t waste your time looking at homes that don’t align with your needs or lifestyle. A buyer’s agent can also help connect you with resources for financing options or payment assistance programs.

Step 4: Look for Homes to Buy

Average timeline: Three days to several months

Now for the fun part: looking for homes to buy! Your real estate agent will have access to all available listings (and then some) that fit your budget and needs through the MLS software, but it’s always helpful to share any homes you’ve already found with them. This will help them better understand your preferences and style. Remember, time is of the essence—if you see one you like online, request a showing from your real estate agent immediately.

Today, many real estate listings have virtual tours and 3D renderings so you can get a really good feel for a property without setting foot inside. While this is a huge time saver, and you may feel comfortable making an offer based on this alone, virtual tours should really be used as a screening tool to further narrow your home search; you usually don’t want to purchase a house without seeing it in person first. And don’t forget about your list of must-haves and deal-breakers!

Step 5: Make an Offer to Buy a Home

Average timeline: One day to two weeks

If your finances are in order and you have a pre-approval letter, you should have no problem making an immediate offer to buy a home you love. There’s no official time frame for a seller to accept or reject your offer, but you’ll typically get a response within 72 hours. However, if a seller is considering multiple offers, you might end up waiting a little bit longer. Once your offer is accepted by the seller, the home will likely go into contract within a few days.

A good real estate agent can help make your offer standout, eliciting a faster response. One way to do this is to put down extra earnest money. Earnest money is essentially a “deposit” on the house put into an escrow account to take it off the market, typically between 1% to 3% of the home’s value. Obviously, the more you put down, the more appealing your offer seems to sellers. Without it, buyers could potentially make offers on multiple homes at the same time and leave sellers out to dry. Fortunately, the earnest money goes toward the down payment or closing costs once the deal goes through! On the other hand, there’s no guarantee you’ll get this money back if it doesn’t.

Another reason this phase of the home-buying process might take longer is if the seller comes back with a counteroffer. A buyer is expected to respond to a counteroffer within 72 hours, but doing so as soon as possible will definitely paint you in a favorable light and move things along more quickly. Your agent will most likely develop a counteroffer plan with you ahead of time.

Step 6: Find a Mortgage Lender for Your Home Loan

Average timeline: One day to two weeks

A mortgage lender can help you decide what type of loan is right for you and your financial situation. They can also help you with different down payment options and strategies. A longer home loan term can mean lower monthly mortgage payments, while some government-backed home loans offer lower down payments upfront.

Again, you don’t have to stick with the same lender who gave your pre-approval—your real estate agent can usually connect you with a trusted mortgage lender. You’ll want to make sure you apply for your home loan as soon as your offer is accepted to close things as quickly as possible.

Step 7: Schedule a Home Inspection, Home Appraisal & Title Search

Average timeline: Two to three weeks

Once the home is under contract, you’ll enter the “due diligence” period—a time frame when you are able to make sure everything is up to code and acceptable, and back out of the deal if not. The most important things during this part of the home-buying journey are the home inspection, home appraisal, and title search.

A home inspection involves a certified inspector conducting a thorough assessment of the home—from the plumbing to the foundation—to see if there are any issues that could cost you money down the road. If there are problems, you can choose to negotiate the price down or ask the seller to have the repairs made as part of the purchase agreement for the house. Some eager home buyers are choosing a “walk-and-talk consultation” instead of a typical home inspection, which could save three or five days. This is where the buyer does a walk-through with a home inspector while they examine any major structural flaws that would be expensive to fix, such as a faulty foundation or an old roof. Some buyers choose to waive the home inspection contingency entirely, to save time and possibly entice sellers to accept their offer over others. However, it’s recommended to never skip the home inspection, as you never know what problems or safety concerns they could uncover! Once the home inspection is complete, you typically have seven days to make a final decision on purchasing the house.

A home appraisal is an unbiased evaluation by a certified appraiser of a home’s current value. The appraiser will visit the house and consider things like the home inspection report, structural issues, size, and neighborhood comparisons. If a home is appraised for less than the asking price, it can affect your mortgage lender’s willingness to back the current loan terms, leaving you to pay the difference or walk away from a home you love. But, you also have the opportunity to negotiate a lower purchase price!

A title search is a process that confirms homeownership and verifies who has the right to sell you the house. The title company will also look for any easements or right-of-ways that may prevent you from completing future renovations, like installing a pool. The end goal is to ensure the seller has the right to sell the home (and legally transfer it to you) and protect your future ownership.

Step 8: Process Your Home Loan

Average timeline: Three days to three weeks

Once you’re under contract on a home and applied for a home loan, your mortgage lender will begin to process your application to approve your mortgage. The loan underwriter will verify all your financial information, like your credit score, bank details, and the info on the home you’re trying to buy.

Being pre-approved puts you in a good position to get your actual mortgage application approved, however, this isn’t always guaranteed. But it will make the loan processing go much quicker, since you’ve already submitted all the necessary paperwork. Regardless, make sure to respond to your lender and their underwriter as quickly as possible to ensure things go smoothly. Once your mortgage application is approved, you’ll receive the “clear to close” notice!

Step 9: Close on Your New Home

Average timeline: Three to 10 days

You’ve almost bought a home! Closing is the final step in the home-buying process and it’s when all parties come together to sign all purchase documents and officially exchange ownership of the property. Typically, all the paperwork is signed in person, with both real estate agents, closing attorneys, and a lender rep. Sometimes, you may be allowed to have a remote signing, but this can add extra time to the process.

Although these happen before the actual signing, there are a couple of other elements considered part of the closing process. You’ll need to review your home loan for accuracy and exact figures, as well as all other documentation. Also, you’ll want to do a final walkthrough of the home you’re buying to make sure nothing has changed from what you agreed to purchase, or that any requested changes have been made.

If everything is finalized and in order, you and the home seller can sign the final paperwork, transfer the necessary funds, and get the keys to your new home.

Congratulations! You’re now a homeowner. Buying a home is a journey that starts well before you even get pre-approval. So, understanding the timeline for buying a house will help you prepare for the process and eventually buy the home of your dreams.

Whether you’re still considering if buying a home is right for you or you’re ready to start your home search today, we can help! If you’re looking to buy a home in Houston, Texas, our team of real estate professionals can help ensure a smooth process.

Alexis Feezel is a results-oriented Marketing Coordinator responsible for developing, implementing, and overseeing all promotional strategies and activities to effectively market clients & listings and maximize sales.